Elasticity of Demand

Tells how drastically buyers will cut back or increase their demand for a good when the prices rises or falls.1. Elastic demand

When demand will change greatly given a small change in price.-We tend to think of wants.

Ex) if movie tickets increase to $25, we are lead to find alternate ways.

More than one

2. Inelastic demand

Your demand for a product will not change regardless of price.We tend to think of needs.

Ex) Milk, gasoline, medicine, salt

Less than 1

3. Unielastic demand

Equal to one1.New quantity-old quantity/ old quantity

2.New price-old price/ old price

3. PED

Equilibrium

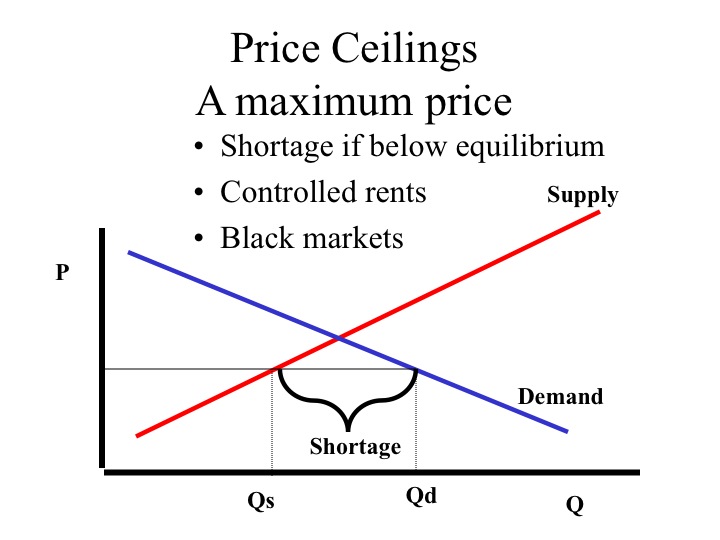

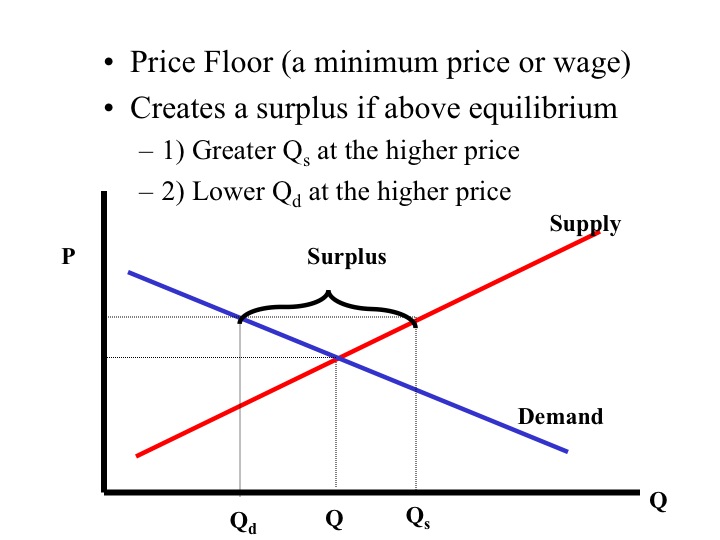

The point at which the supply curve and demand curve intersect. The point that they insect at means that an economy is using their resources efficiently.Shortage- QD>QS

Surplus- QS>QD

Price ceiling

Government imposed limit on how high you can be charged or service.

Price floor

Government imposed minimum on how low a price can be charged for a service.Ex) $7.25 minimum wage

Total Revenue- Price x Quantity

Marginal Revenue

Additional income from selling an additional unit of a good.

Fixed cost

A cost that does not change no matter how much is produced.

Ex) rent, mortgage

Variable cost

A cost that changes and fluctuates.Ex) water bill (how much you use)

Marginal cost- New total cost - old total cost

Spend the cost, revenue is what you bring in.Total cost- TFC+TVC=TC

Average total fixed cost- AFC + AVC

Average Fixed Cost- TFC/Quantity

Average Variable Cost- TVC/Quantity

Total Variable Cost- Quantity x AVC

I like how you color-coded each section, and that you included many examples in the form of pictures as an addition to the notes you provided. It may be a good idea to find a video on how to solve supply practice problems to accompany your data tables. :)

ReplyDeleteYour blog is very informative and precise on what the topic is about.

ReplyDelete