Demand

The quantities that people are willing and able to buy at various prices.

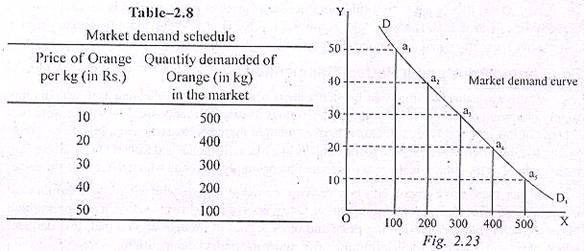

The Law of Demand

An inverse relationship between price and quantity demanded.

Demand Schedule and Demand Curve

Displays the relationship of Price and Quantity demanded.

Increase in demand - shift to the right.

Decrease in demand - shift to the left.

What causes a "change in quantity demanded"? (ΔQD) Δ in price

What causes a "change in demand"? (ΔD)

1) Δ in buyer's taste (advertising)

2) Δ in the number of buyers (population)

3) Δ in income

A. Normal goods - goods that buyers buy more of when their income rises.

B. Inferior goods - goods that buyers buy less of when their income rises.

4) Δ in the price of related goods.

A. Substitute goods - goods that serve roughly the same purpose to buyers.

ex) Coca Cola and Pepsi

B. Complimentary goods - goods that are often consumed together.

ex) Gasoline and automobile, fries and ketchup.

5) Δ in expectations - thinking about the future.

Supply

The quantities that producers or sellers are willing and able to produce or sell at various prices.

The Law of Supply

There is a direct relationship between price and quantity supply. (Price increases, quantity increases)

Supply Schedule and Supply Curve

What causes a "change in supply"? ( ΔQS) Δ in price

What causes a "change in supply"? ( ΔS)

1) Δ in weather

2) Δ in technology

3) Δ in taxes or subsidies

4) Δ in cost of production

5) Δ in number of sellers

6) Δ in expectations